Sending a child abroad for higher education is a monumental milestone for any Indian family. However, the academic journey is often accompanied by a complex, high-stakes financial labyrinth. Between exorbitant university tuition fees, soaring living expenses, and the volatile exchange rate of the Indian Rupee, parents can easily lose lakhs of rupees to invisible banking margins. By deploying strategic international student education loans and advanced forex hacks, you can aggressively protect your family’s hard-earned capital.

Smart Finance Disclaimer: The banking regulations, loan interest rates, and Tax Collected at Source (TCS) policies discussed in this guide are strictly for educational purposes and based on the latest Indian financial guidelines. Forex markets and government tax mandates under the Liberalised Remittance Scheme (LRS) fluctuate rapidly. Always consult your chartered accountant or a dedicated bank relationship manager before executing high-value international remittances.

Under the current LRS rules, international remittances for education funded by a formal education loan attract a highly reduced TCS of just 0.5% on amounts exceeding ₹7 Lakhs. If funded through personal savings, the TCS jumps to 5%.

Never use a standard Indian credit or debit card to pay massive university tuition portals online. Standard cards will apply a crippling 3.5% foreign transaction fee plus 18% GST, which can instantly add thousands of dollars to your tuition bill.

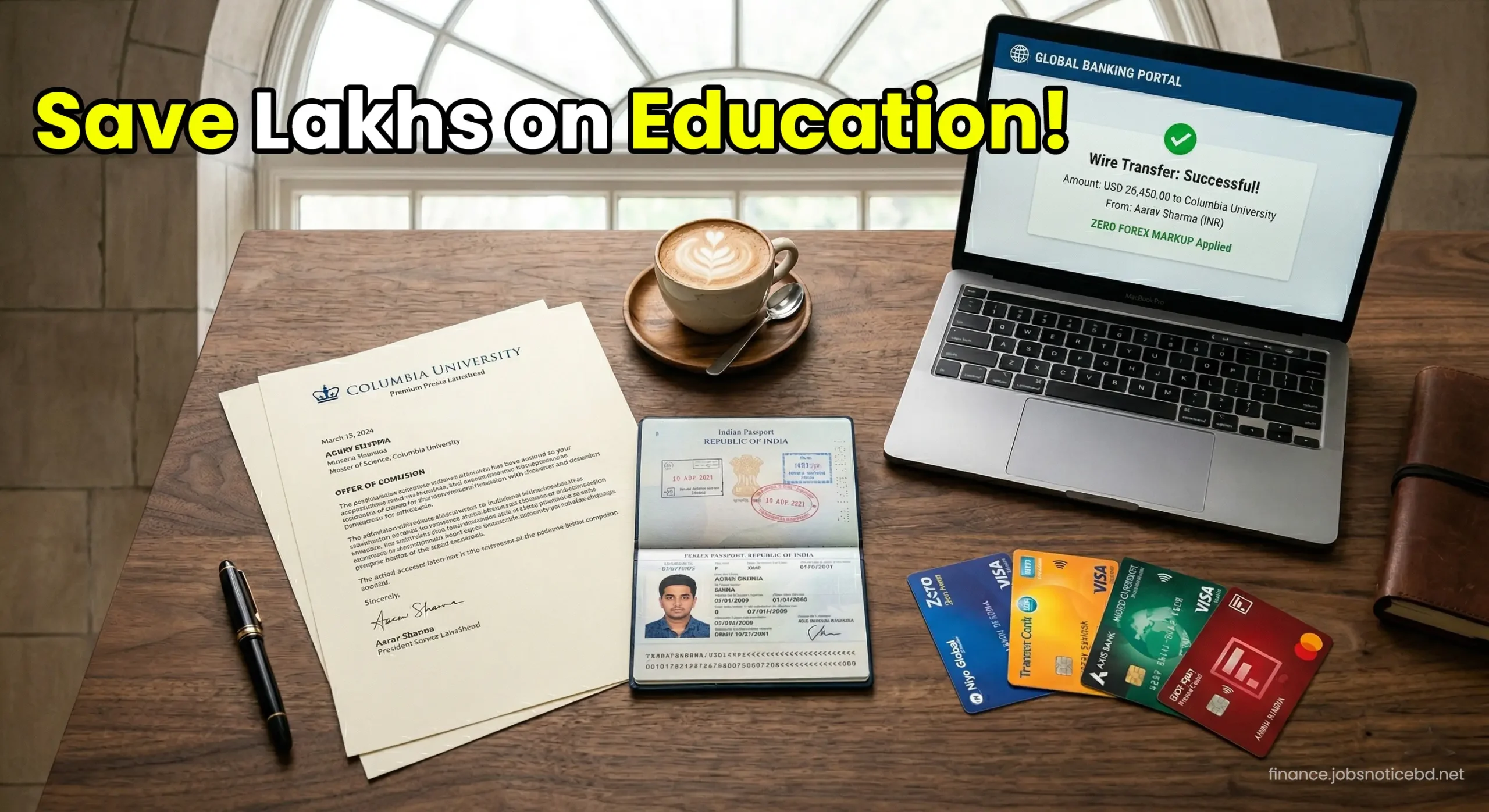

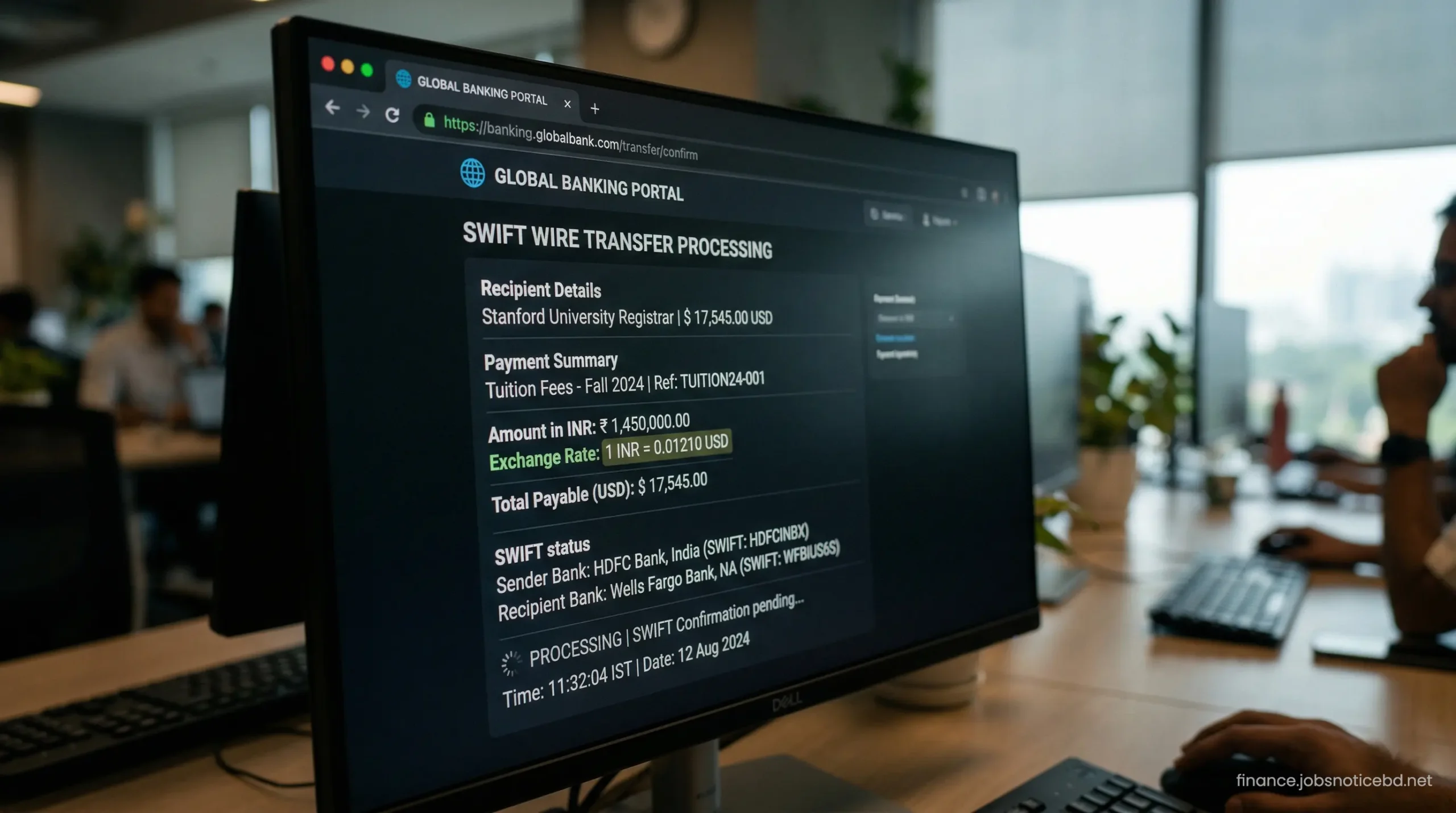

For large, bulk payments like semester tuition and on-campus housing, traditional SWIFT wire transfers processed through specialized forex platforms offer the most aggressive, near-interbank exchange rates compared to standard retail banks.

The True Financial Burden of Studying Abroad

When calculating the cost of a master’s degree in the US or UK, most families simply multiply the dollar amount by the current Google exchange rate. This is a critical mathematical error. Retail banks never provide the mid-market exchange rate to individual consumers. Instead, they apply a currency conversion spread, effectively selling you foreign currency at a premium.

Furthermore, standard banking instruments are littered with hidden fees. Whether you are paying application fees, booking flight tickets, or simply transferring monthly living allowances, you are constantly bleeding capital. Understanding how to mitigate these hidden forex markup charges is the absolute foundation of international student finance.

To survive this financial gauntlet, Indian families must transition from basic savings accounts to optimized corporate-grade financial tools. This begins with structuring the initial funding correctly through specialized education loans that offer inherent tax advantages.

Structuring International Education Loans

Securing an education loan is no longer just about borrowing money; it is a vital tax-saving strategy. Under the Liberalised Remittance Scheme (LRS), the Indian government mandates a Tax Collected at Source (TCS) on foreign remittances. If you send more than ₹7 Lakhs in a financial year from your personal savings for education, a 5% TCS is locked up with the government until you file your income tax returns.

However, if the remittance is funded directly by an approved education loan from an Indian financial institution, the TCS rate plummets to a mere 0.5% for amounts exceeding ₹7 Lakhs. This massive reduction ensures your capital remains liquid and available for actual educational expenses rather than being trapped in government tax credits.

Additionally, Section 80E of the Income Tax Act allows the co-applicant (usually the parent) to claim an absolute, limitless deduction on the interest paid toward the education loan for up to eight years. This effectively reduces the actual cost of borrowing significantly.

| Funding Source (Over ₹7 Lakhs) | Applicable TCS Rate | Tax Deduction Benefit (Sec 80E) |

|---|---|---|

| Personal Savings / Fixed Deposits | 5.0% | None |

| Approved Education Loan | 0.5% | Unlimited interest deduction |

| Non-Education Remittance | 20.0% | None |

Bypassing Forex Markups on Tuition Payments

Once the loan is approved, the next challenge is actually moving the money to the foreign university. Many universities provide a direct payment gateway on their student portal. Attempting to pay a $20,000 tuition fee through this portal using a standard Indian debit card is a catastrophic mistake.

Instead, parents must utilize specialized B2B forex remittance platforms or approach the forex division of their bank directly. By initiating a SWIFT wire transfer, you can lock in a highly negotiated exchange rate. Always ask the bank for their specific “Student Remittance Rate,” which is traditionally lower than their standard retail rate.

Furthermore, when executing the SWIFT transfer, clearly specify that the purpose code falls under educational remittance. This ensures the correct, lower TCS rate is applied automatically by the bank’s compliance department, preventing unnecessary tax blockages.

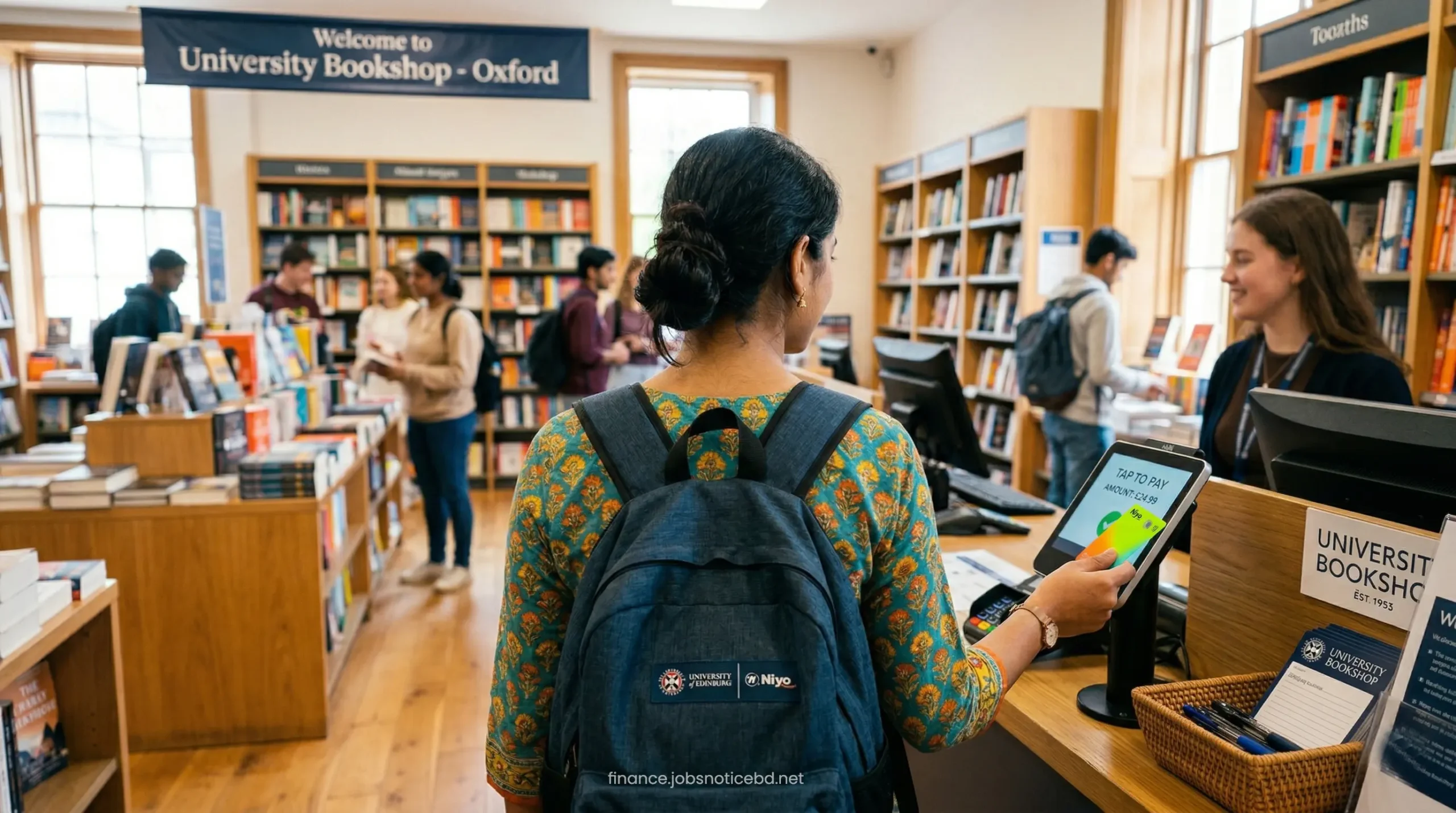

The Multi-Currency Card Strategy for Students

Tuition is only half the battle; managing daily living expenses is where most students lose money to banking friction. Equipping a student with a standard Indian card means they will pay an extra 4% every time they buy groceries or ride the subway.

To optimize daily spending, students must carry dedicated, zero-markup plastic. As detailed in our ultimate guide to forex cards, multi-currency prepaid cards allow parents to load funds in INR while the Indian Rupee is performing strongly, locking in the conversion rate instantly.

| Student Card Option | Forex Markup | Best Use Case on Campus |

|---|---|---|

| Niyo Global (Student Account) | 0% | Daily groceries, coffee shops, and local public transit. |

| BookMyForex Student Card | 0% (Locked Rates) | Budget control and protecting against sudden INR depreciation. |

| Add-on Premium Credit Card | ~2% (Offset by points) | Flight bookings, emergency medical bills, and security deposits. |

Fintech solutions like Niyo Global are incredibly popular among the student demographic because they allow parents to seamlessly transfer funds via UPI directly into the student’s linked INR account. The student can then spend the money internationally with absolute zero markup.

Never let your child open a foreign bank account until they have physically arrived on campus and verified the student banking perks. In the interim, provide them with an international forex card. More importantly, ensure they are trained to aggressively decline Dynamic Currency Conversion (DCC) at local terminals. Selecting INR on a foreign machine will instantly trigger a devastating 5% to 7% markup, entirely defeating the purpose of carrying a zero-markup card.

Pre-Departure Financial Checklist

The financial preparation phase includes more than just securing loans and loading cards. Much like understanding how to pay the US visa fee from India without absorbing unnecessary charges, managing the logistical details before departure is critical.

First, ensure the student’s Indian bank accounts have international usage explicitly enabled for POS, E-commerce, and ATM withdrawals via the mobile app. Second, upgrade the student’s mobile plan to include a basic international roaming pack. Receiving crucial banking OTPs (One Time Passwords) on an Indian SIM card while abroad is absolutely mandatory for executing digital transactions.

Finally, always mandate that the student carries a secondary backup card. If their primary forex card is lost, skimmed, or swallowed by an international ATM, waiting weeks for a replacement from India is not a viable option. A secondary card kept locked in their dorm room safe guarantees uninterrupted financial liquidity.

Empowering the Next Generation

Funding an international education is a massive undertaking, but it does not need to be a financially leaky process. The banking industry relies heavily on parental anxiety to push expensive, unoptimized remittance products. By educating yourself on the mechanics of LRS, TCS, and forex spreads, you completely neutralize these predatory practices.

Deploy specialized education loans to optimize your tax liabilities. Execute bulk tuition payments via highly negotiated SWIFT wire transfers. Finally, empower your child with zero-markup multi-currency cards for their daily survival. By mastering these financial logistics, you ensure that every single rupee you invest goes directly toward your child’s education and future, rather than disappearing into a bank’s profit margin.

Frequently Asked Questions (FAQ)

1. Can I use a premium travel credit card to pay international university tuition?

While technically possible, it is highly discouraged. Most universities charge an additional 2% to 3% convenience fee for accepting credit card payments. When combined with the bank’s forex markup (if not using a zero-markup card), you will lose an astronomical amount of money. Always use a SWIFT wire transfer for tuition.

2. Does the 0.5% TCS on education loans apply to living expenses as well?

Yes. If the approved education loan specifically covers living expenses as part of the total disbursement package, the funds remitted abroad for accommodation and food will also enjoy the highly reduced 0.5% TCS rate under the LRS guidelines.

3. How long does a SWIFT wire transfer take to reach a foreign university?

A standard SWIFT wire transfer typically takes between 48 to 72 business hours to reflect in the university’s foreign bank account. Always initiate the transfer at least a week before the university’s final deadline to account for compliance checks and intermediary bank delays.

4. Can an Indian student apply for a credit card once they land in the US or UK?

Yes, but it is difficult initially because they lack a local credit history. Programs like Nova Credit can sometimes translate an Indian credit score, or students can apply for specialized student credit cards (like Discover Student in the US) to slowly build their local credit profile.

5. What happens to the unused foreign currency on a prepaid forex card when the student returns?

Upon returning to India, the remaining foreign currency balance on the prepaid forex card can be easily encashed or refunded back into the parent’s linked Indian bank account at the prevailing buying exchange rate set by the card issuer.