The United Arab Emirates represents the ultimate playground for luxury shopping, fine dining, and architectural marvels. However, the glittering allure of Dubai can quickly turn into a financial nightmare for Indian tourists who carry the wrong plastic. The conversion spread between the Indian Rupee (INR) and the UAE Dirham (AED) is a massive profit center for traditional banks. If you are not equipped with the optimized financial tools, you will unknowingly surrender up to 5% of your total vacation budget to invisible banking fees before you even leave the Dubai Mall.

Smart Finance Disclaimer: The credit card features, forex markup rates, and reward structures detailed in this comparative guide are strictly for educational purposes and are based on the latest 2026 data. Bank policies and currency conversion spreads fluctuate rapidly. Always consult HDFC Bank or Equitas/DCB Bank directly to verify the most current terms before applying for these financial products.

Dubai is predominantly a cashless society. Optimize your wallet by using the Niyo Global card for absolute zero-markup retail shopping, and reserve the HDFC Regalia for luxury hotel bookings where securing high reward points offsets the standard markup.

When purchasing gold in Deira, merchants often impose an extra 2% to 3% surcharge for credit card payments. You must withdraw physical AED from a local ATM to secure the absolute lowest per-gram gold rate.

Dubai International Airport (DXB) has some of the most expensive terminal food in the world. Leveraging a card with a complimentary Priority Pass membership guarantees you free dining and rest areas during long transit layovers.

The UAE Dirham (AED) Conversion Challenge

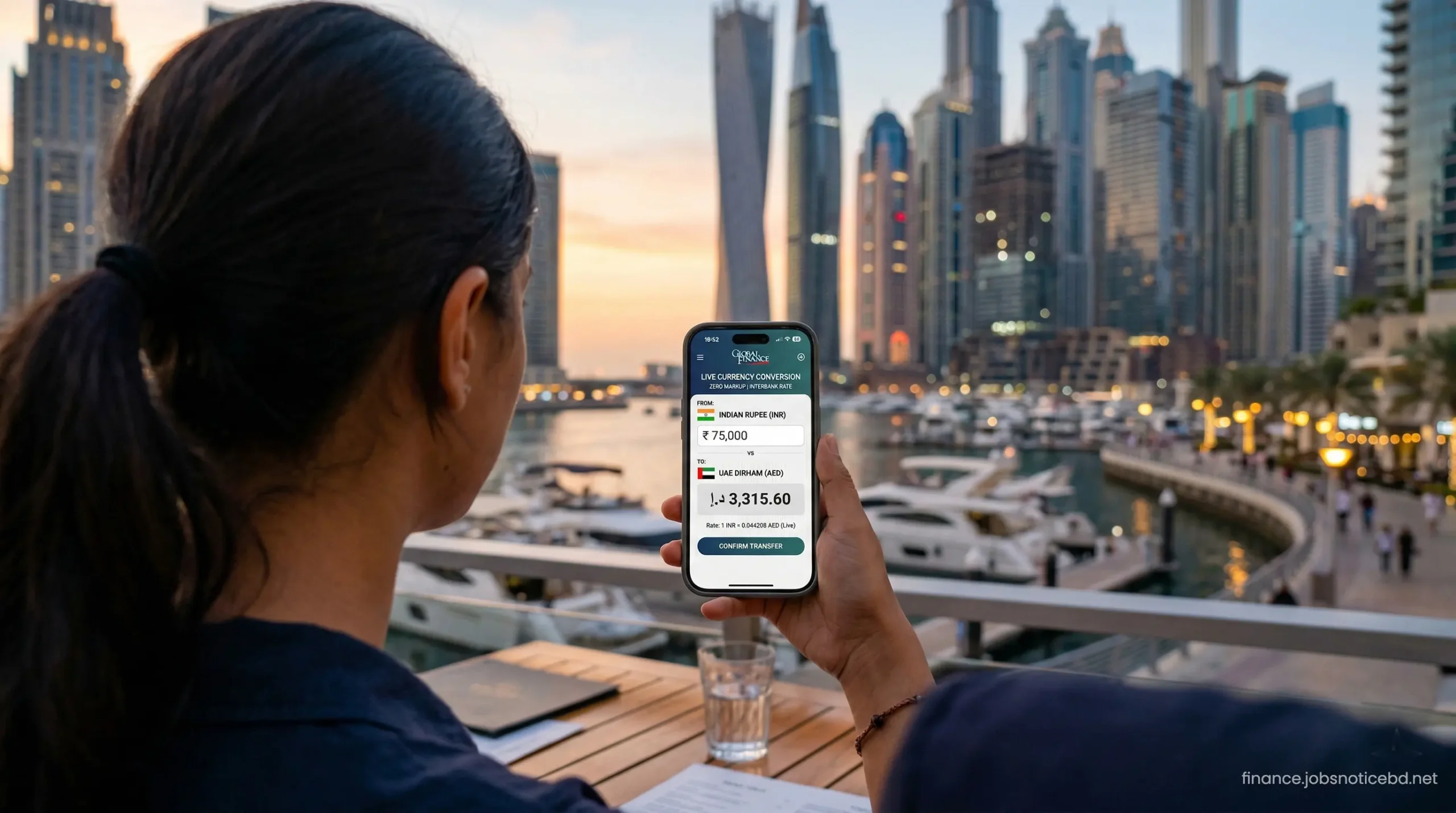

The UAE Dirham is pegged to the US Dollar, making it a highly stable and powerful currency. When Indian travelers swipe a standard debit or credit card in Dubai, the transaction rarely converts directly from INR to AED. Instead, the network often executes a double conversion: INR to USD, and then USD to AED. Each hop across a currency border incurs a fractional spread, severely diluting your purchasing power.

Furthermore, standard Indian bank cards automatically slap a massive 3.5% fee on top of this conversion. Discovering the reality of these hidden forex markup charges upon returning home is a painful realization for many travelers. To survive financially in the UAE, you must deploy specialized travel cards designed to bypass these predatory conversion architectures entirely.

In the premium segment, two titans dominate the discussion for Indian travelers heading to the Middle East: the fintech disruptor, Niyo Global, and the legacy powerhouse, HDFC Regalia VIP. Choosing the correct weapon for your wallet depends entirely on your specific spending habits.

Niyo Global: The Fintech Disruptor in Dubai

The Niyo Global card, usually issued in partnership with Equitas Small Finance Bank or DCB Bank, is an INR-based, multi-currency prepaid/savings account. Its primary value proposition is simple and devastatingly effective: absolute zero forex markup on all international transactions.

When you swipe the Niyo Global card for a dinner at the Burj Al Arab, the exact Visa exchange rate is applied instantly. There are no hidden spreads, no delayed settlement shocks, and no 18% GST levied on markup fees because the markup is mathematically zero. You simply load Indian Rupees via UPI or IMPS into the linked app, and you are ready to spend in Dubai immediately.

Additionally, the Niyo Global account offers high-interest rates on the loaded INR balance while you travel. However, its primary weakness lies in its lack of premium lifestyle perks. It does not offer lucrative reward points for luxury spends, nor does it provide a comprehensive Priority Pass for international VIP lounge access.

HDFC Regalia VIP: The Luxury Traveler’s Choice

The HDFC Regalia VIP is a traditional, premium line-of-credit product designed for high-net-worth individuals. Unlike Niyo, the Regalia is not a zero-markup card by default. It typically carries a standard forex markup of around 2% (which is still significantly lower than standard 3.5% entry-level cards).

So why is it highly recommended for Dubai? The magic of the HDFC Regalia lies in its aggressive reward multiplier system. While you pay a 2% markup upfront, the massive reward points you generate on international spending effectively neutralize that fee. When optimized correctly, the net return on the Regalia can actually exceed the savings of a zero-markup prepaid card.

Furthermore, the Regalia offers unmatched travel security. If you are renting a luxury sports car in Dubai or placing a security hold at a five-star resort like Atlantis The Palm, a true credit card is mandatory. Prepaid cards like Niyo are frequently rejected by international merchants for security deposits.

Head-to-Head: Core Feature Comparison

To determine the absolute superior financial instrument for your UAE vacation, we must dissect their core metrics side-by-side. The following comparison highlights where each card excels in the grueling environment of international luxury travel.

| Feature / Metric | Niyo Global (Savings/Prepaid) | HDFC Regalia VIP (Credit) |

|---|---|---|

| Forex Markup Fee | 0% (Absolute Zero) | 2% + GST (Offset by points) |

| Annual Holding Fee | Free (Zero joining/annual fee) | ₹2,500 (Waived on milestone spend) |

| Reward Points Ecosystem | Virtually Non-Existent | High (Excellent travel redemption) |

| Hotel Security Deposits | Frequently Rejected | Universally Accepted |

Real-World Spend Test: The Dubai Shopping Festival

To truly understand the financial impact, let us simulate a high-value purchase. Assume you are attending the Dubai Shopping Festival and purchase luxury electronics and designer apparel totaling exactly 10,000 AED. At a hypothetical exchange rate of 1 AED = ₹22.50, the base value is ₹225,000.

If you execute this massive transaction with a standard Indian debit card featuring a 3.5% markup, the bank will add ₹7,875 in markup fees, plus ₹1,417 in GST. Your total cost skyrockets to ₹234,292. You have lost nearly ₹10,000 purely to banking friction.

Now, let us examine how our two premium contenders handle this exact same 10,000 AED transaction.

| Spend Simulation (10,000 AED) | Niyo Global Card | HDFC Regalia VIP |

|---|---|---|

| Base Conversion Amount | ₹225,000 | ₹225,000 |

| Bank Forex Markup + GST | ₹0 | ₹5,310 (2% + 18% GST) |

| Estimated Reward Value | ₹0 | ₹6,000+ (In flight vouchers) |

| Net Effective Cost | ₹225,000 | ₹224,310 (If points redeemed properly) |

The table reveals a fascinating dynamic. For the average traveler who wants straightforward savings without managing point ecosystems, Niyo is undefeated. However, for the meticulous optimizer who routinely redeems points for premium cabin flights, the Regalia actually yields a mathematically superior net return.

If you plan to buy gold at the Deira Gold Souk, merchants will heavily penalize credit card swipes. You need physical Dirhams. Never use the HDFC Regalia to withdraw cash at an ATM in Dubai—it triggers massive cash advance fees and instant 40% APR interest. Instead, load your Niyo Global account, walk up to a local Emirates NBD ATM, and withdraw physical AED. You will bypass the massive credit card interest trap entirely.

Airport Lounge Access at DXB

Dubai International Airport (DXB) is a massive transit hub, and layovers can be exhausting. Access to premium VIP lounges transforms this gruelling experience into a luxurious extension of your vacation. Here, the HDFC Regalia asserts absolute dominance.

The Regalia VIP provides complimentary Priority Pass membership, granting you and often an add-on guest free access to elite international lounges worldwide, including the opulent Marhaba lounges at DXB. You receive complimentary hot meals, premium beverages, and high-speed Wi-Fi, saving you significant airport dining costs.

The Niyo Global card offers extremely limited, strictly domestic lounge access within India. It is useless for securing VIP entry while transiting through international terminals. If airport comfort is a priority for your family, relying solely on a basic fintech card is a strategic error.

Furthermore, when comparing the broader ecosystem, executives traveling to the UAE for business should also evaluate the best corporate travel credit cards in India, which offer even higher tiers of luxury travel insurance and advanced expense tracking over consumer cards like the Regalia.

Final Verdict: The Ultimate Travel Wallet Setup

The debate between Niyo Global and HDFC Regalia should not end with choosing just one. The financially elite Indian traveler carries both. They serve fundamentally different, yet highly complementary, purposes in a perfectly optimized travel ecosystem.

As detailed in our ultimate guide to forex cards, you must use the HDFC Regalia VIP to book your Emirates flights, secure your deposit at the Burj Khalifa, and pay for luxury dining to hoard massive reward points. Simultaneously, you must deploy the Niyo Global card for your daily retail shopping at the mall, automated Metro payments, and vital physical cash withdrawals at local ATMs.

By wielding both instruments precisely where they excel, you extract maximum value from the banking system. You eliminate unnecessary friction, protect your capital from greedy exchange spreads, and experience the unparalleled luxury of Dubai with absolute financial supremacy.

Frequently Asked Questions (FAQ)

1. Can I use the Niyo Global card to pay for a rental car in Dubai?

It is highly risky. Premium car rental agencies in Dubai require a substantial security deposit. They strongly prefer, and often mandate, traditional embossed credit cards like the HDFC Regalia. A prepaid card like Niyo may be rejected outright at the rental counter, leaving you stranded.

2. Does the HDFC Regalia charge a fee for ATM cash withdrawals in the UAE?

Yes, and it is catastrophic. Withdrawing cash on any credit card triggers a “Cash Advance.” HDFC will charge an immediate flat withdrawal fee plus a massive annualized interest rate that begins compounding the very second the cash leaves the ATM. Never use a credit card for ATM withdrawals.

3. Is my money safe in the Niyo Global account if I lose the physical card?

Yes. Niyo provides an advanced mobile application that allows you to instantly lock the card, block specific transaction types (like international POS or ATM), and reset your PIN. Your funds remain secure in the underlying bank account (Equitas or DCB) while a replacement card is issued.

4. Do I need separate travel insurance if I have the HDFC Regalia?

The Regalia offers complimentary insurance, but it often has strict activation clauses (like booking the flights with the card) and lower coverage limits. If you are extending your trip to Europe, you must procure dedicated Schengen travel insurance to meet strict embassy medical requirements.

5. Will paying in INR at the Dubai Mall save me money?

Absolutely not. If a merchant in Dubai offers to bill your card in Indian Rupees, they are using Dynamic Currency Conversion (DCC). This allows their acquiring bank to apply a terrible, highly inflated exchange rate. Always aggressively decline DCC and insist on being billed in the local UAE Dirham (AED).