Every time you swipe your standard Indian credit or debit card on foreign soil, a silent financial mechanism activates, siphoning money directly from your travel budget. Most travelers remain completely unaware of these deductions until they return home and review their bloated monthly statements. This guide exposes the hidden architecture of foreign transaction fees and teaches you exactly how to bypass them on your next international journey.

Smart Finance Disclaimer: The financial strategies and fee structures detailed below are for educational purposes. Banking terms, foreign exchange rates, and taxation rules fluctuate continuously. Always consult your issuing bank directly and review their most recent schedule of charges before executing international transactions.

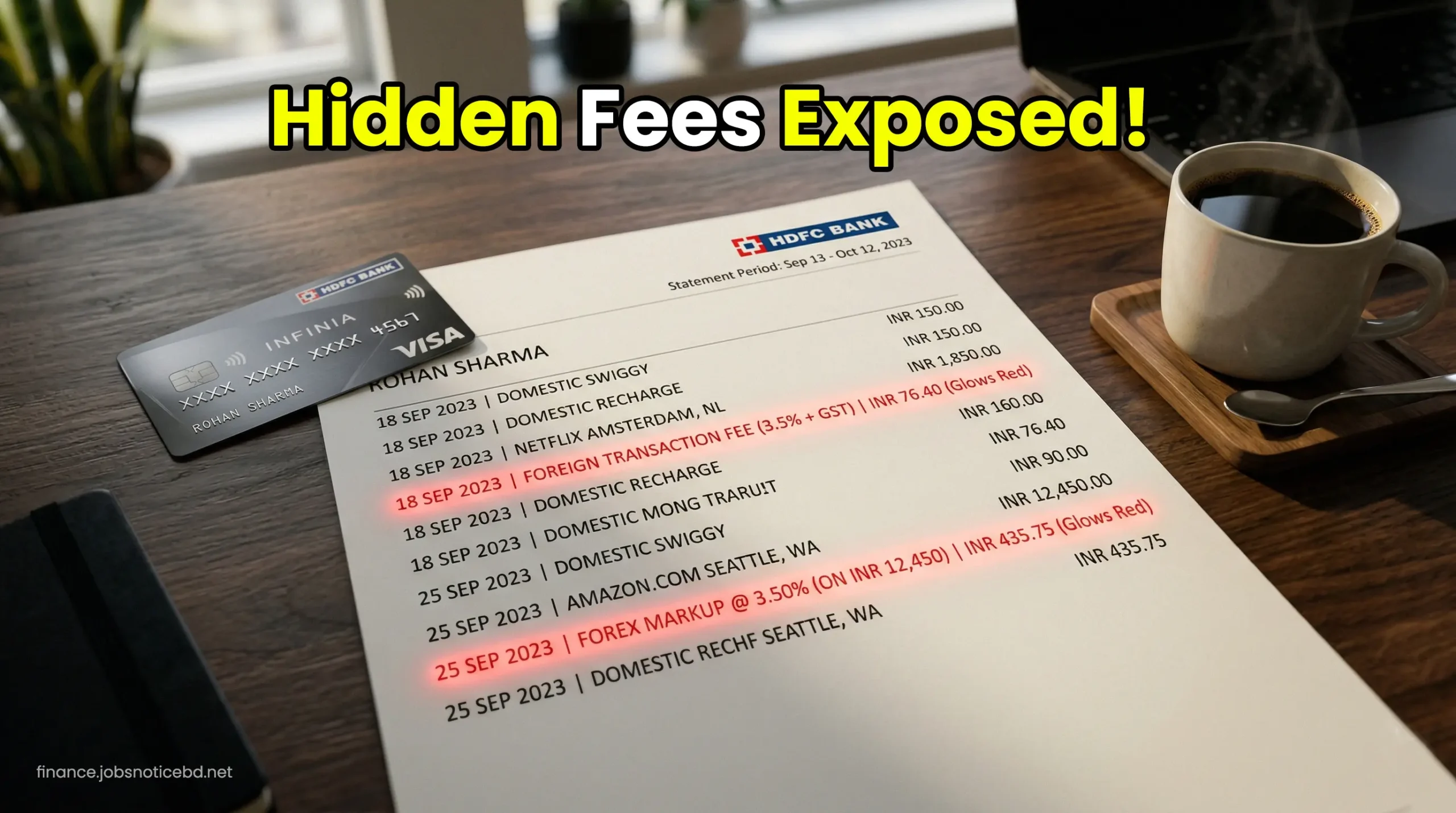

A standard 3.5% forex markup fee does not exist in isolation. The Indian government levies an additional 18% GST directly on that markup amount, pushing your actual penalty closer to 4.13% on every single international swipe.

Using a credit card to withdraw cash from a foreign ATM is the most expensive financial mistake you can make. It triggers an immediate flat cash advance fee plus exorbitant interest rates that compound daily from the exact moment of withdrawal.

You can legally bypass these hidden charges by transitioning your travel wallet to specialized financial instruments. Securing dedicated zero forex markup credit cards eliminates bank-side conversion fees entirely.

The Anatomy of a Foreign Swipe

When you purchase a coffee in Paris or a souvenir in Dubai, the transaction amount is originally processed in the local currency. Your Indian bank must then convert your native Rupees into that foreign currency to settle the merchant’s account. This conversion process is where the financial extraction occurs.

Banks do not perform this currency conversion out of goodwill. They apply a surcharge known as a Foreign Currency Markup Fee. For standard credit and debit cards issued in India, this fee typically ranges between 2.5% and 3.5% of the total transaction value.

This fee is rarely displayed on the merchant’s card machine at the point of sale. Instead, it is silently calculated and tacked onto your final credit card statement days later. Consequently, travelers operating on strict budgets often find themselves facing unexpected financial shortfalls upon returning to India.

Understanding the Tax Multiplication Effect

The financial penalty of using a standard card abroad is not limited to the bank’s markup percentage. The Indian taxation system amplifies this cost. The Goods and Services Tax (GST) is legally mandated on all financial services, including currency conversion fees.

Currently, the GST rate applied to forex markup is 18%. This tax is not applied to the total transaction value, but strictly to the markup amount itself. For example, if you spend ₹100,000 internationally and your bank charges a 3.5% markup (₹3,500), the 18% GST is applied to that ₹3,500.

This adds another ₹630 to your bill. Therefore, your “hidden” fee for a single ₹100,000 transaction instantly becomes ₹4,130. Over the course of a two-week international vacation, these invisible charges can easily consume the equivalent cost of a return flight ticket.

| Transaction Breakdown (₹100,000 Spend) | Standard Bank Card (3.5% Markup) | Zero Forex Markup Card |

|---|---|---|

| Base Transaction Amount | ₹100,000 | ₹100,000 |

| Bank Forex Markup Fee | ₹3,500 | ₹0 |

| GST on Markup (18%) | ₹630 | ₹0 |

| Total Amount Billed to You | ₹104,130 | ₹100,000 |

The Illusion of Dynamic Currency Conversion (DCC)

Forex markup is charged by your home bank in India. However, there is a secondary, far more predatory fee engineered by foreign merchants. This trap is known as Dynamic Currency Conversion (DCC). It is presented to you at the checkout counter disguised as a helpful convenience.

When you insert your card into a foreign terminal, the machine may recognize your card as Indian. It will politely ask if you prefer to be billed in the local currency or in Indian Rupees (INR). Selecting INR feels safe because you immediately see the final amount in a familiar currency.

This is a catastrophic financial mistake. By selecting INR, you give the foreign merchant’s acquiring bank permission to dictate the exchange rate. They will invariably use a terrible, highly inflated rate, often baking a 5% to 7% profit margin directly into the transaction. You must aggressively decline DCC and always choose to pay in the local currency.

Hidden Dangers of International ATM Cash Advances

While tap-to-pay is prevalent globally, carrying physical currency is still mandatory for tipping, small vendors, and local transport. The method you use to procure this cash dictates how much money you will lose to the banking system. Walking up to a foreign ATM with a standard credit card is a financial hazard.

Credit card companies do not view ATM withdrawals as standard purchases; they categorize them as “Cash Advances.” The moment the machine dispenses the cash, you are hit with a flat cash advance fee, typically ranging from $5 to $10. But the bleeding does not stop there.

Unlike regular purchases that enjoy a 45-day interest-free grace period, cash advances begin accruing massive interest instantly. This annualized percentage rate (APR) can exceed 40%. Within days, a simple cash withdrawal can multiply into a significant debt burden.

To completely eliminate cash advance interest rates, never insert your primary credit card into an ATM abroad. Instead, procure a dedicated multi-currency prepaid forex card. Load your travel budget onto this card via a bank transfer before leaving India. When you withdraw cash using this prepaid card, you only pay a tiny, fixed international ATM access fee, bypassing the credit card interest trap entirely.

The Cross-Currency Conversion Penalty

Even travelers who utilize prepaid forex cards can fall victim to hidden fees if they do not understand cross-currency charges. A multi-currency card allows you to load specific currencies, such as US Dollars or British Pounds, into separate wallets on the same card.

A cross-currency fee is triggered when you swipe your card in a country where you do not hold the native currency in your wallet. For example, if you loaded your card exclusively with Euros but decide to take a weekend train to Switzerland (which uses Swiss Francs), a penalty applies.

When you purchase a coffee in Zurich, the bank must internally convert your Euro balance into Swiss Francs to pay the merchant. Banks charge a cross-currency markup for this internal transfer, usually around 2% to 3.5%. To avoid this, always ensure your prepaid card supports the exact currency of your destination and load it appropriately before crossing borders.

Shielding Your Corporate Travel Expenses

The impact of hidden forex markups is magnified exponentially for business travelers. Companies dispatching employees abroad for conferences and client meetings face massive budgetary leaks if their staff relies on standard corporate cards with heavy markups.

Every international hotel booking, client dinner, and taxi ride becomes 4% more expensive. Financial controllers must intervene and issue optimized instruments to traveling employees. Upgrading the company wallet to best corporate travel credit cards in India instantly seals this leak, retaining thousands of rupees per trip within the company’s profit margins.

| Hidden Fee Type | Typical Charge Range | How to Bypass It Completely |

|---|---|---|

| Forex Markup | 2.5% – 3.5% + GST | Use an elite Zero Forex Markup Credit Card. |

| DCC (Dynamic Conversion) | 5% – 7% Exchange Rate Inflation | Always decline INR; pay in local currency. |

| Cash Advance Interest | Flat Fee + up to 40% APR instantly | Never use credit cards at ATMs; use debit/prepaid. |

| Cross-Currency Surcharge | 2.0% – 3.5% | Load exact local currency on multi-currency cards. |

Protecting Your Entire Travel Investment

Eliminating hidden banking fees is only one facet of a secure international travel strategy. Your capital must also be protected against unforeseen geopolitical events, medical emergencies, and severe logistical disruptions. A sudden medical evacuation in Europe can bankrupt an uninsured traveler instantly.

While upgrading your financial tools, you must simultaneously upgrade your risk management. Before applying for your visa, it is mandatory to secure robust cheapest travel insurance for Indian senior citizens visiting Europe. Ensure your policy provides comprehensive cashless hospitalization features.

Do not assume the complimentary travel insurance bundled with your credit card is sufficient. Often, these built-in policies have severe limitations regarding age limits and pre-existing medical conditions. A dedicated, standalone travel medical policy is a non-negotiable requirement for international peace of mind.

Executing a Zero-Fee Financial Strategy

The banking industry relies heavily on consumer ignorance to generate massive profits through hidden foreign transaction fees. By educating yourself on the anatomy of cross-border payments, you instantly strip the banks of this unfair advantage.

Prior to your next departure, audit your current wallet. Discard the standard debit cards that leak 4% on every swipe. Upgrade your primary spending tool by comparing the best travel card for Dubai or your specific destination. Pair an elite credit card with a reliable multi-currency forex card.

When you stand at a foreign checkout counter and aggressively decline the DCC prompt, you are actively protecting your wealth. Travel is an investment in human experience; do not let hidden banking markups dilute the value of your journey. Equip yourself properly, spend strategically, and explore the globe with absolute financial confidence.

Frequently Asked Questions (FAQ)

1. Why doesn’t my bank tell me about the Forex Markup fee before I travel?

Banks detail the forex markup fee within the exhaustive terms and conditions document provided when you first open the account or receive the card. They are not legally required to send individual alerts before each international swipe, relying on the fact that most consumers do not read the fine print.

2. Is the Visa or Mastercard exchange rate the same as the Google rate?

It is incredibly close. The Visa and Mastercard network rates are wholesale interbank rates. They typically include a virtually microscopic spread (usually less than 0.5%) above the pure mid-market Google rate. It is the absolute best conversion rate accessible to retail consumers.

3. Can I claim the GST paid on Forex Markup back?

For individual leisure travelers, the 18% GST levied on the forex markup fee is a sunk cost and cannot be claimed back. However, GST-registered business entities utilizing corporate credit cards for official travel can often claim Input Tax Credit (ITC) on these specific banking service charges.

4. If I use an Indian card on an international website while sitting in India, do I pay markup?

Yes. Physical location is irrelevant. If the payment gateway or the merchant acquiring bank is registered outside of India, the transaction is processed as an international cross-border payment. Your Indian bank will automatically apply the standard forex markup fee.

5. How do I know if a foreign ATM is going to charge me an access fee?

Most international ATMs are legally required to display a warning screen detailing their specific access fee before dispensing cash. You must accept this fee on the screen to proceed. If the fee is too high, simply cancel the transaction and find an ATM affiliated with the Global ATM Alliance.